Page 225 - KWAP_AR2022

P. 225

FoR BetteR RetuRns Annual Report 2022 223

notes to the

financial statements

for the year ended 31 december 2022

33. FINANCIAL RISK (CONTINUED)

(d) Credit risk (continued)

(i) Credit risk management (continued)

in the determination of an improvement of the credit risk of a modified financial asset with the loss allowance

measured at lifetime ecl to the extent of reverting to the loss allowance measured at 12-months ecl,

the grading system (i.e. investment and non-investment grade) was employed to assess improvement in credit

quality of a modified financial asset.

the said financial assets are monitored until the loss allowance is subsequently remeasured at the lifetime

ecl.

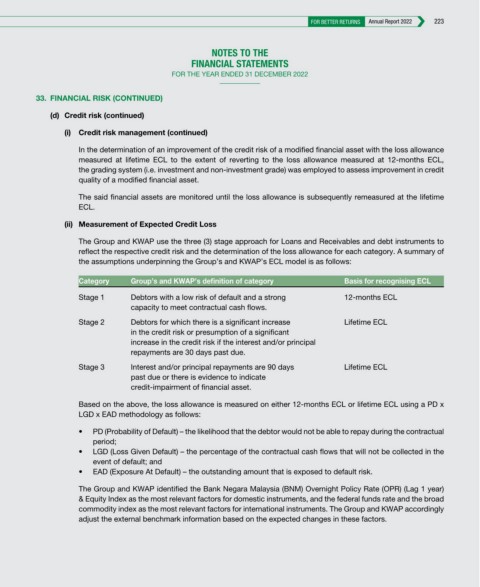

(ii) Measurement of Expected Credit Loss

the group and KWap use the three (3) stage approach for loans and receivables and debt instruments to

reflect the respective credit risk and the determination of the loss allowance for each category. a summary of

the assumptions underpinning the group’s and KWap’s ecl model is as follows:

Category Group’s and KWAP’s definition of category Basis for recognising ECL

stage 1 debtors with a low risk of default and a strong 12-months ecl

capacity to meet contractual cash flows.

stage 2 debtors for which there is a significant increase lifetime ecl

in the credit risk or presumption of a significant

increase in the credit risk if the interest and/or principal

repayments are 30 days past due.

stage 3 interest and/or principal repayments are 90 days lifetime ecl

past due or there is evidence to indicate

credit-impairment of financial asset.

based on the above, the loss allowance is measured on either 12-months ecl or lifetime ecl using a pd x

lgd x ead methodology as follows:

• PD (Probability of Default) – the likelihood that the debtor would not be able to repay during the contractual

period;

• LGD (Loss Given Default) – the percentage of the contractual cash flows that will not be collected in the

event of default; and

• EAD (Exposure At Default) – the outstanding amount that is exposed to default risk.

the group and KWap identified the bank negara malaysia (bnm) overnight policy rate (opr) (lag 1 year)

& equity index as the most relevant factors for domestic instruments, and the federal funds rate and the broad

commodity index as the most relevant factors for international instruments. the group and KWap accordingly

adjust the external benchmark information based on the expected changes in these factors.